Mortgage rates are currently at their highest point in over twenty years, making it tougher for homebuyers today compared to the past. Many still remember when rates were historically low just two years ago, allowing them to afford more. However, today’s buyers face a big problem: there aren’t enough homes for sale, which has driven up prices quickly. On top of this, there’s high inflation, and wages have barely grown for decades. As a result, people have less buying power than they did twenty years ago. This has led to a significant affordability crisis as rates go up. Andy Walden, a vice president at Black Knight, says that the housing market now relies more on low-interest rates to maintain home prices than it did in the past.

Mortgage Rates Comparison

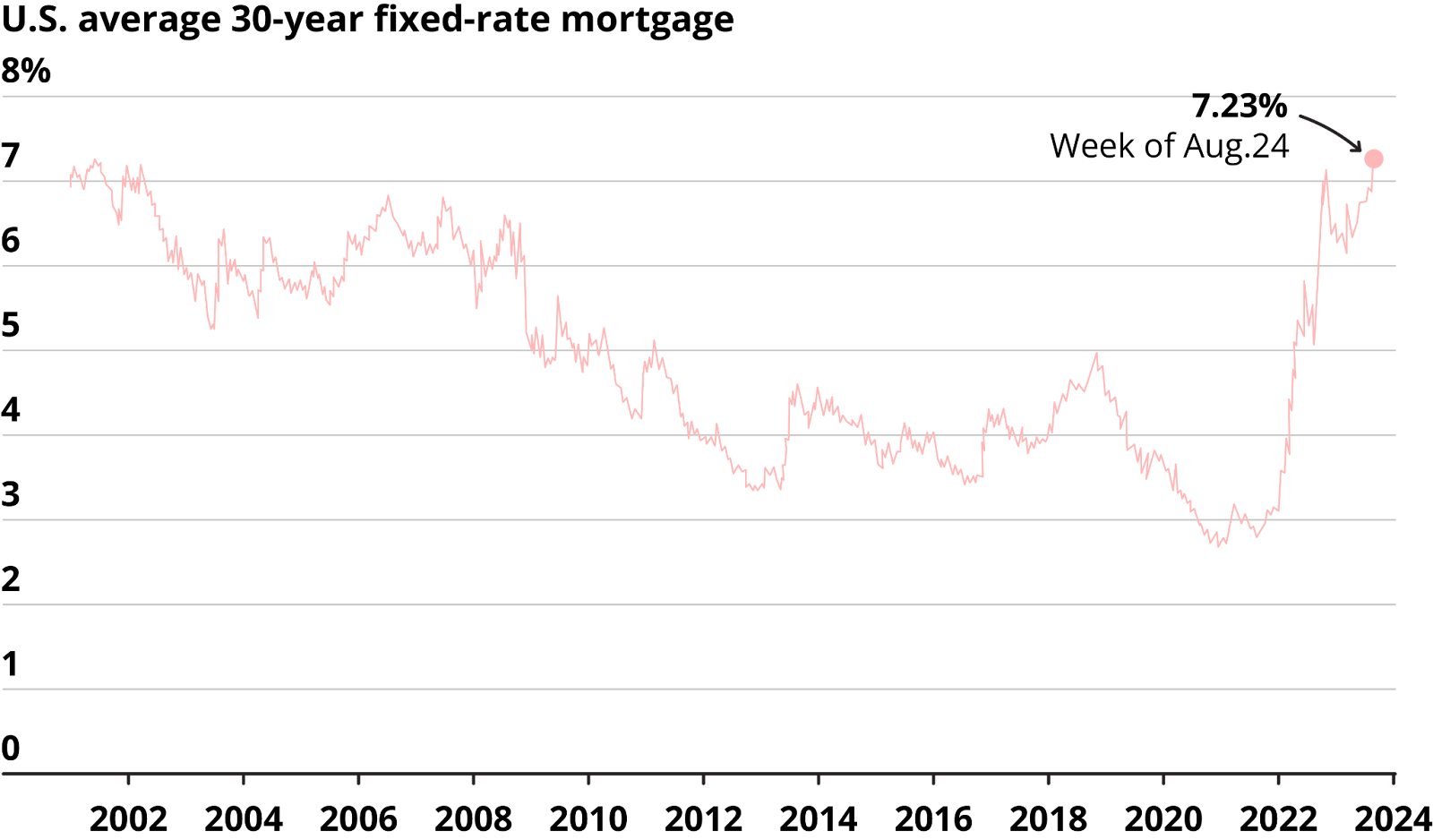

Mortgage rates are on the rise. Last week, the average rate for a 30-year fixed mortgage was 7.18%, and it went up to 7.24% the week before. This marks the third consecutive week with rates above 7%, something we haven’t seen since April 2002. But back in 2002, even though rates were above 7%, they had been at that level for most of the previous ten years. The housing market was quite different then. To give you an idea, between 1992 and April 2002, rates averaged 7.66%. They started to decline after that, averaging 6.03% until around mid-2006 when the housing bubble reached its peak. Len Kiefer, a deputy chief economist at Freddie Mac, explained that in the early 2000s, the Federal Reserve was worried about the possibility of deflation. During that time, the Core PCE price index only increased by 1.4% from March 2001 to March 2002. In contrast, today, the Federal Reserve is more concerned about inflation, with the Core PCE price index showing a 4.1% year-over-year increase.

Today’s homebuyers are having a very different experience. The Federal Reserve has been rapidly increasing its benchmark interest rate over the last year and a half. Mortgage rates have gone up too, but this is after they dropped to record lows of under 3% for over a year during the pandemic. This low rate triggered a buying frenzy and a surge in homeowners refinancing their mortgages. During this period of record-low rates, almost nobody had a mortgage rate higher than 6%. In fact, a study by Redfin in June found that 91.8% of US homeowners had a mortgage with an interest rate below 6%. Moreover, 82.4% had a rate below 5%, and 62% had a rate below 4%. Andy Walden explains that all of this is because of how homebuyers, and consequently home prices, behave when interest rates are falling, a trend that’s been going on for about 40 years.

Supply And Demand Comparison

Lately, homeowners with low mortgage rates are holding onto their homes and not selling, creating what’s called a “lock-in effect.” This has resulted in a shortage of homes available for resale and a decrease in sales. The homes that are available for sale are often older and less appealing to buyers. As a result, many homebuyers are turning to the new home market, which has boosted sales there. Builders are trying to keep up by building more homes, but it’s not enough to make up for the shortage. Demand for homes is still strong, especially among millennials, who are now in their prime years for buying homes. However, even small increases in mortgage rates are making it difficult for many of them to afford homes. As a result, the number of home purchase applications has been declining as rates have gone above 7%. In contrast, twenty years ago, the situation was different. Despite an eight-month recession in 2001, home sales remained steady, and consumer confidence was strong. Mortgage rates were falling, and there was a growing demand for homes, which is the opposite of what’s happening today. The housing market then saw higher levels of home construction, both for new and existing homes. Mortgage applications for home purchases were on the rise, indicating steady demand, which is unlike the current situation. Overall, back then, rising home values made buying homes a good investment, even as stock prices were falling.

TFC Team

thefirm.sg